.jpg?#)

How will the Iran war affect the global economy?

AS the war with Iran enters its second week, the most immediate and tragic costs are measured in lives lost. Yet economists are obliged to consider another dimension: the economic consequences. These, too, could be significant – though their distribution across the world economy will be uneven. Some countries will bear substantial costs. For others, the impact may prove surprisingly modest.

The heaviest burden will inevitably fall on the region itself. History offers a guide. During the 12-day war last summer, Israel’s economy contracted by around 1 per cent in the second quarter. If the conflict is short-lived, a fall in output of a similar order of magnitude would seem plausible for both Israel and the Gulf economies.

A more prolonged conflict would almost certainly inflict a deeper economic wound. Output would be disrupted, investment postponed and tourism curtailed. Iran’s economy will be hit even harder. Based on the impact of wars elsewhere, GDP is likely to fall by more than 10 per cent – although Iran itself last published official GDP data in 2024.

But what of the global economy? Directly, the Middle East matters less than is often assumed. The Gulf economies account for only around 2-3 per cent of global GDP. Even a severe regional downturn would therefore have limited direct consequences for world output.

Chokepoints

Instead, the key risks surround disruptions to the supply of goods that economies in the region send to the rest of the world. Crises such as this have a habit of revealing chokepoints that were previously hidden. For example, Qatar produces around 40 per cent of the world’s helium, which is used in the production of semiconductors. The region is also a significant producer of ammonia and nitrogen, which are key ingredients in many synthetic fertilizer products. The real transmission channel, though, is energy.

Around a quarter of global seaborne oil passes through the Strait of Hormuz, along with roughly one-fifth of liquefied natural gas (LNG) shipments. Any disruption to transit through this narrow chokepoint has immediate consequences for global energy markets. Unsurprisingly, oil and gas prices have jumped over the past week as shipments through the Strait have collapsed.

In economic terms, the mechanism through which such shocks operate is straightforward. Higher energy prices alter what economists call a country’s terms of trade – the price of its exports relative to its imports. When energy prices rise, income is transferred from energy-importing countries to energy exporters.

The economic consequences of that transfer depend on three factors: whether a country is a net importer or exporter of energy; how large and persistent the price rise proves to be; and how governments, households and businesses respond to the shift in income.

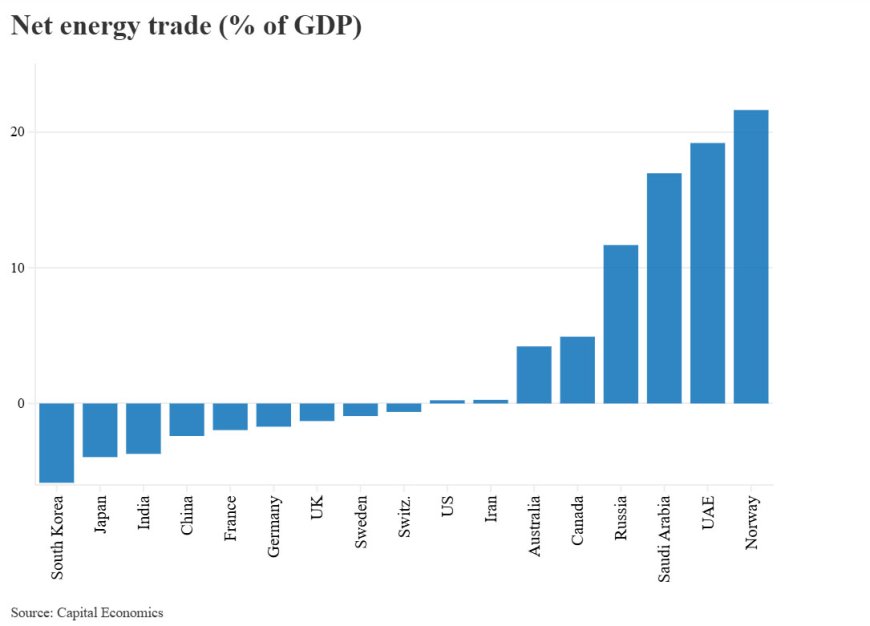

The obvious winners are large net energy exporters outside the Gulf whose ability to sell abroad is unaffected. Countries such as Norway, Russia and Canada stand to benefit the most from higher energy prices. (See Chart below.)

At the other end of the spectrum sit economies where energy imports account for a large share of GDP. This group includes countries such as South Korea, Taiwan, Japan, India and China, as well as most European economies, including France, Germany and the UK.

The United States sits somewhere in the middle. Thanks to the shale revolution, the country has shifted from being one of the world’s largest energy importers to a modest net exporter. In aggregate, that means the US economy as whole now benefits slightly from higher global energy prices – although the gains will be unevenly distributed.

The scale and persistence of the energy shock will ultimately determine the macroeconomic impact. For energy-importing economies, the main transmission channel is likely to be via inflation. Higher oil and gas prices raise the import bill faced by households and firms, squeezing real incomes and eroding purchasing power.

If the spike in prices proves brief, most advanced economies should be able to absorb the shock. Even if oil prices remain in the region of $70-80 per barrel and gas prices stay close to current levels, inflation in 2026 in Europe and Asia would probably be only around 0.5 percentage points higher than pre-conflict forecasts. The effect on real GDP growth would be small.

In countries where energy subsidies remain extensive and government finances are already shaky, higher energy prices could unsettle bond markets.

A more severe scenario would be different. If oil prices climbed towards $100 per barrel and remained elevated throughout the year – accompanied by a comparable rise in natural gas prices – inflation might be roughly one percentage point higher and GDP growth perhaps 0.25–0.4 percentage points lower. Those central banks that are still loosening policy – notably the Bank of England – would also become less comfortable with cutting interest rates further.

Even so, such a shock would be far smaller than the one that followed Russia’s full-scale invasion of Ukraine, when Europe faced an abrupt and dramatic disruption to its energy supplies. The current conflict, unless it escalates dramatically, is unlikely to provoke large-scale fiscal rescue packages from governments.

Emerging markets and the US

In several emerging markets, the impact of higher energy prices is softened by government subsidies. In such cases, it would be the state rather than households and businesses that would bear the initial increase in costs. That will cushion the blow to growth in the short term but come at the expense of weaker public finances.

For most emerging economies this will be manageable: fiscal positions are generally stronger than they were a couple of decades ago. But in countries where energy subsidies remain extensive and government finances are already shaky, higher energy prices could unsettle bond markets. Economies such as Egypt and Tunisia appear particularly vulnerable. A surge in global energy prices could also destabilize Pakistan’s fragile economy.

One final consequence of the conflict is that it is likely to reinforce a broader pattern in the world economy: the relative strength of the United States. Having moved from a large net importer of energy to a modest exporter, the US is now less exposed to global energy shocks than many of its peers. While American households will still face higher fuel prices, energy producers – and their investors – stand to benefit.

The movements in energy prices seen so far are unlikely to transform the US economic outlook for this year. But they may complicate the task of the Federal Reserve. A renewed rise in fuel inflation would give policymakers another reason to proceed cautiously when considering interest-rate cuts.

None of this diminishes the human cost of conflict. But from an economic perspective, the effects – while real – are likely to be uneven and, at the global level, manageable. Indeed, if energy prices remain contained, the world economy may absorb the shock with less disruption than many fear.